You opened this expecting to read about Mars. Rockets. Colonisation timelines. Elon Musk's vision. Maybe a debate about whether any of it will happen.

That article exists. Thousands of versions of it exist.

This is not that article.

This article is about something much older, much quieter, and in the long run, much more expensive than Mars.

It is about production.

Not as a concept. As the physical, time-bound, irreducible process by which the future either gets built — or does not.

Mars is the frame. Production is the argument. And the argument begins, as most economic arguments do, with money.

"The best way to predict the future is to invent it."

Alan Kay · Computer scientist, Xerox PARC

But before you can invent the future, someone has to finance it. And before it can be built, someone has to actually build it.

These are not the same thing.

The market sells the ticket. Production builds the rocket. The economy on Mars does not yet exist.

This is what financial optimism looks like at its most extreme: a departure board for destinations that have no infrastructure, no supply chain, no precedent for human habitation at scale. Mars at $750,000 a ticket. Status: Now Boarding.

The image is deliberately absurd. But the logic it illustrates is not. Markets routinely price journeys before the roads exist to take them. The question — always the same question — is how long the gap lasts between the ticket price and the infrastructure required to honour it.

Before we get to Mars, we need to understand what money actually is, what production actually requires, and why these two things are not as connected as financial markets tend to assume.

Before the theoryThe Long Way to Production

Over two decades, I watched capital become forests, highways, mines, factories and supply chains. Different countries. Different cultures. Different political systems.

The same physical law, every time.

I did not understand for some time that these experiences were connected. They seemed like separate chapters — forestry, a desert crossing, gold mining, textile factories. It was only later that I noticed they were all describing the same constraint, appearing in different forms, on different continents, in different industries.

In Latvia, I watched loggers work through mosquitoes, horseflies, ticks and rain. Chainsaws running from first light. Trees that do not always fall where expected. Sometimes they fall on the people cutting them.

Financial markets have never cut down a tree. Someone still has to stand beneath it.

Later, to start a business in West Africa, we bought a Mitsubishi Pajero in Riga, loaded it with more than 400 kilograms of tools, spare parts and equipment, and drove south.

Europe. The Mediterranean. The Sahara. Eventually, Abidjan.

Crossing the Sahara changes your understanding of systems. Every decision becomes physical. Fuel range. Water. Tyre pressure in heat. Weight distribution. Spare parts for failures that happen in places where the nearest workshop is two days away. Logistics stops being a supply chain term. It becomes the difference between arriving and not arriving.

The Sahara taught me that every system has a physical minimum. Below that minimum, no amount of planning closes the gap.

For more than a decade, I drove regularly from Riga to Warsaw. At first, the route passed demolition sites. Then foundations. Then cranes. Then office towers. Then entire districts where nothing had stood before. Month after month, year after year, I watched capital become concrete.

The highway between Kaunas and Warsaw changed too. Not overnight. It accumulated — lane by lane, junction by junction, across years of construction. Production rarely announces itself. It accumulates.

In Ghana, I joined an alluvial gold mining operation. In Uzbekistan, I saw where a T-shirt actually begins. Not in a marketing department. Not in a design studio. In a cotton field.

Every step is physical. Every step takes time. Every step can fail. The brand is the last thing that gets added — and the first thing the consumer sees.

The same law, every time. Production is always physical before it is financial.

Act IMoney

A claim on production — nothing more.

Money is a claim on production. Not on gold. Not on government promise. At its most basic level, money is a social agreement that this token can be exchanged for something that was actually made — grown, extracted, assembled, coded, transported, built.

When that agreement functions, money is extraordinarily useful. It prices things that would otherwise be impossible to compare. It allows resources to flow toward where they are needed without requiring personal trust between strangers.

But the agreement has a structural weakness.

The amount of money in circulation can be increased by policy. The amount of production in the world cannot be increased by decree.

Central banks create liquidity. That liquidity flows through the financial system. It finds its way into assets — equities, real estate, private companies, and increasingly, into the valuations of businesses that do not yet produce what their price implies.

Global monetary context (2024 estimates):

~$105TGlobal M2 money supply

~$110TGlobal GDP

~$109TGlobal public debt

Sources: IMF World Economic Outlook 2024, BIS. Figures are estimates, rounded for illustration.

These three numbers sitting in rough proximity to each other are not a coincidence. They reflect decades of deliberate monetary expansion. The result: when money is abundant and cheap, markets do not just price what exists today. They price what they believe will exist tomorrow — and they price it now, in full, with confidence.

NASDAQ Composite 1995–2002. The technology survived. ~$5 trillion did not.

The internet was real. It did reshape global commerce, communication, and culture, exactly as the optimists believed. But in March 2000, 86% of newly public technology companies were unprofitable at the moment of peak valuation. The market had priced the productive capacity of the internet before the internet had built it. The technology arrived. The timeline did not.

The internet was not a mistake. The marginal buyer at 5,049 was.

Money can increase nominal value. Scarcity can increase perceived value. Narrative can increase market value. A concession grants rights to gold still in the ground. A valuation prices a Mars economy before the first city exists.

But only production increases real capacity.

"The stock market is there to serve you, not to instruct you."

Warren Buffett · Chairman, Berkshire Hathaway

The market's job is to offer prices, not to define reality. A price is an offer. It is not proof that the underlying thing exists, functions, or will perform as implied.

Markets price trees. Nature doesn't care.

When desire becomes a production constraint.

Three industries. Three different mechanisms. The same constraint.

Rolex estimated annual sales CHF billions 2020–2025. The product tells time. The market sells status, scarcity and future resale value.

Rolex does not maximise output. It constrains it — deliberately, structurally, permanently. From CHF 4.42 billion in 2020 to an estimated CHF 11 billion in 2025, revenue grew not because Rolex built more factories, but because the brand maintained — and in some periods tightened — the production ceiling that makes each watch more desirable than the last.

Mechanism: controlled supply — pricing power comes from production discipline, not from the price alone.

Illustrative hypercar category expansion index 2005–2025. 25× expansion since 2005.

In 2005, a million-dollar production car seemed irrational. The Bugatti Veyron was widely described as an engineering exercise with no commercial logic. It turned out to be the opening act of a category. The hypercar market expanded approximately 25 times between 2005 and 2025 — not because money wished it into existence, but because manufacturers built the production systems, the supply chains, the service networks, and the client relationships required to sustain it.

Mechanism: physical capacity limits — the market did not create the hypercar category. Production created it. The market followed.

2005 → 2026. From one $1M car to a global hypercar ecosystem. Scarcity backed by production is an asset. Scarcity without production is a promise.LVMH annual revenue € billions 2005–2025. Luxury is not a basic need. Yet it creates products, stores, logistics, employment and cash flow.

From €13.9 billion in 2005 to €86.2 billion at peak in 2023, LVMH built the most successful luxury production empire in history — not by manufacturing desire, but by manufacturing the products that desire attaches to. Narrative alone does not build a luxury empire. It requires ateliers, supply chains, quality control systems, retail infrastructure, and institutional expertise accumulated over decades.

Mechanism: institutional expertise built over time — even the most sophisticated production-backed luxury businesses are not immune to the gap between desired price and actual productive demand.

Demand is not a factory. It is a signal that a factory might be worth building.

Act IIProduction

The Pyramids. Rome. Atlantis. Burj Khalifa. NEOM / The Line. Who pays for the dream? Is history repeating?

Capital accelerates systems. It cannot replace them.

Every civilisation has eventually confronted the same question: who pays for the dream, and who actually builds it?

The Pyramids were not a financial instrument. They were a production achievement — tens of thousands of workers, over decades, moving stone through a logistics system of extraordinary complexity. The financing was organised by a state. The building was done by people with tools in heat.

NEOM's "The Line" is being financed by a sovereign wealth fund at a scale that would have seemed impossible a generation ago. The financing is real. The city is not yet. The gap between those two facts is where this essay lives.

Factories do not compound at the speed of optimism.

A new semiconductor fabrication facility for advanced chips takes approximately four to five years to build and qualify — and that is with unlimited capital, experienced teams, and full regulatory cooperation. TSMC's manufacturing edge was built over forty years of institutional learning. You cannot buy forty years. You can only spend them.

Alluvial gold mining, West Africa. The price on the screen assumes the infrastructure already works.

On the ground — Ghana

I learned this distinction not from a textbook but from terrain.

In Ghana, I was involved in an alluvial gold mining operation. Temperatures regularly climbed above 40°C. By midday, the heat became oppressive. Dust mixed with sweat. Diesel fumes hung over the site. Every piece of machinery worked at its limit — and so did every person on it.

On a screen, gold is a price that changes every second. A line chart. A number responsive to central bank policy and geopolitical risk, updated in real time from trading floors thousands of kilometres away.

On the ground, it is something else entirely.

Sometimes the only relief from the heat was the river. We knew that upstream, artisanal miners used mercury during gold recovery. And yet after hours in that heat, the water still felt irresistible.

One day I cut my leg on a submerged rock. It looked insignificant. It wasn't. In that climate, the wound refused to heal. Day after day it stayed inflamed. Only after I returned to Latvia, months later, did it finally close.

That experience taught me something no spreadsheet ever could.

Production moves at the speed of heat, machinery, logistics, biology — and people. A concession grants you the right to extract gold that is still in the ground. The market may price that concession generously. But the gold does not move until the system is built to move it. And the system does not build itself.

Nominal gold price USD/oz — 1971 to January 2026. All-time high: $5,602.22, January 28, 2026.

Gold moves when the system stops trusting itself.

From $41 per ounce at Bretton Woods to $5,602 at the January 2026 all-time high. This chart is not primarily a story about gold. It is a story about the recurring gap between monetary expansion and productive capacity.

Gold spikes at the same moments every time: when inflation outpaces wages, when financial systems face systemic stress, when the gap between money supply and productive output becomes too wide for markets to ignore.

U.S. national debt 1970–2026. $37 trillion. A claim on future production.

At $37 trillion in U.S. national debt alone, the gap between what has been promised and what can be produced is not abstract. It is structural. And it is moving in one direction.

Gold does not produce anything. That is precisely why it holds value when production systems lose credibility.

Money has never grown a tree. It has only changed who owns the forest.

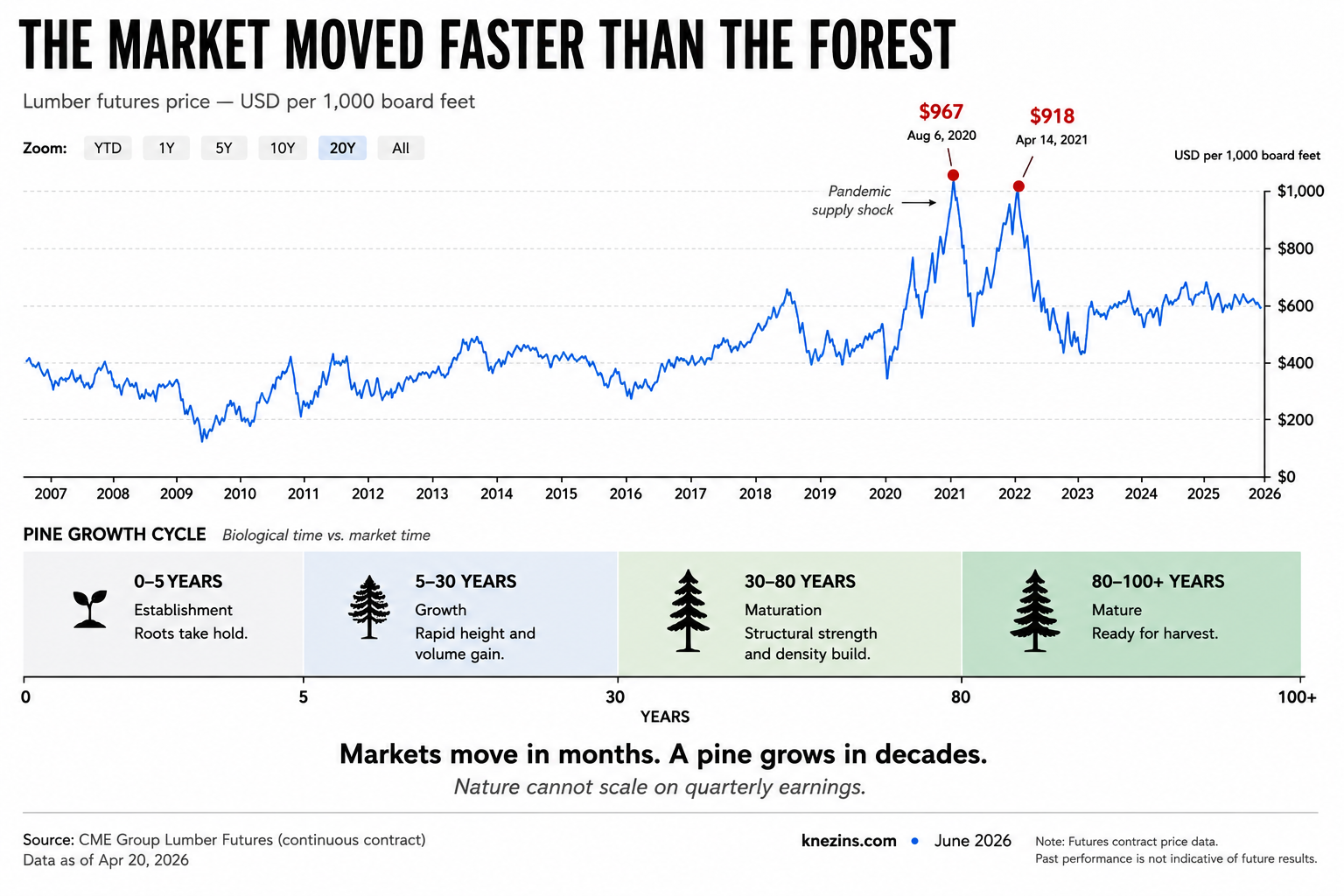

A mature pine, suitable for structural timber, takes between eighty and one hundred years to grow. The market can price the chair made from its wood. It can price the timber, the forest, the land, the concession rights to harvest it decades from now. All of those prices are real. They move when central banks speak.

Lumber futures price USD per 1,000 board feet 2007–2026. Markets move in months. A pine grows in decades.

Every stock chart moves faster than an oak tree.

Lumber prices spiked to $967 per thousand board feet in August 2020 and again to $918 in April 2021. The forests did not respond. A pine planted in response to a price spike does not become structural timber for a generation.

Production obeys biology, physics, and time. Markets obey expectations. Money obeys policy. Confusing these three is where bubbles begin.

You can own the concession. You can own the forest. You can own the field. None of it produces anything until the system is built to process it.

"A complex system that works is invariably found to have evolved from a simple system that worked."

John Gall · Systemantics, 1975

No production system of meaningful scale was assembled all at once. Tesla's Gigafactory took years to reach designed output. SpaceX's launch cadence compounded over more than a decade of iteration. These are not marketing timelines. They are the actual pace at which complex systems develop reliability.

Act IIIMars

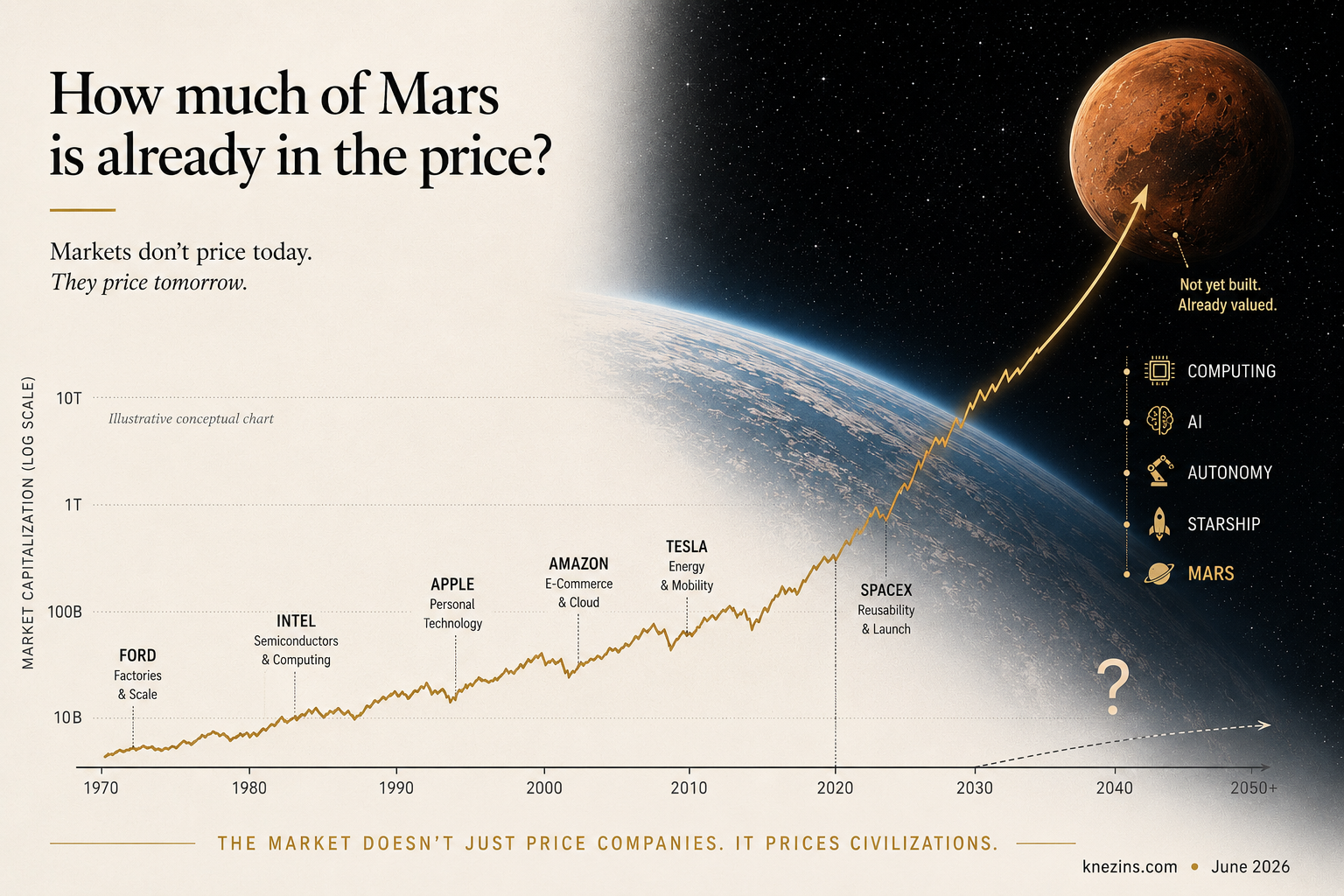

Market capitalisation log scale 1970–2050+. Markets don't price the present. They price expectations. The market doesn't just price companies. It prices civilisations.

People do not buy Mars. They buy the belief in future productivity.

This chart ends with a question mark. That question mark is the most important piece of financial information in it.

Mars is not a market. There are no Mars consumers, no Mars GDP, no Mars supply chain. And yet Mars is priced. Indirectly — through the valuations of companies whose stated mission includes building the infrastructure to reach it. SpaceX's most recent reported valuations have placed it in the range of $200–$350 billion. That figure cannot be explained by current launch revenues and Starlink subscriptions alone. A significant portion is a bet on something that does not yet exist.

This is not irrational. It is how financial markets are designed to work. The risk is when the expectation price moves faster than the production reality. With Mars, the gap is — by definition — interplanetary.

The Mars Test: imagine the cities already exist.

Forget the rockets. Forget the timeline debate. Imagine Mars already has a permanent human settlement of one hundred thousand people. Now think about what they need.

What they need

The production reality

Breathable atmosphere, pressurised structures

Must be manufactured on-site or shipped from Earth at extreme cost

Water extraction and purification

Entirely dependent on local extraction systems that don't yet exist

Food production — indoor, at scale

No existing model at this scale in closed environments

Electricity generation and storage

Solar at reduced efficiency; nuclear the only reliable option

Steel, concrete, raw materials

Either imported at prohibitive cost or produced locally from scratch

Medical infrastructure

Dependent on supply lines 54–401 million km long

Communication networks

3–22 minute signal delay eliminates real-time Earth support

Transport — surface and orbital

Requires fuel production on Mars itself to be economically viable

Every item on that list is a production problem. Not a vision problem. Not a financing problem.

If Mars is ever inhabited, it will not survive because someone priced the future correctly. It will survive because someone built the production capacity to keep people alive.

"The future is not predictable, but futures can be imagined."

Dennis Gabor · Nobel Prize in Physics, 1971

Imagining the future is easy. Financing the imagination is harder. Building the production capacity that makes the imagined future real — that is the constraint every civilisation has eventually confronted.

The rocket is real. The economy is still a projection.

So the serious question is not whether Mars is possible. It is: how much of that possibility is already in the price — and what happens if the production reality arrives on a different schedule?

Act IVCapital

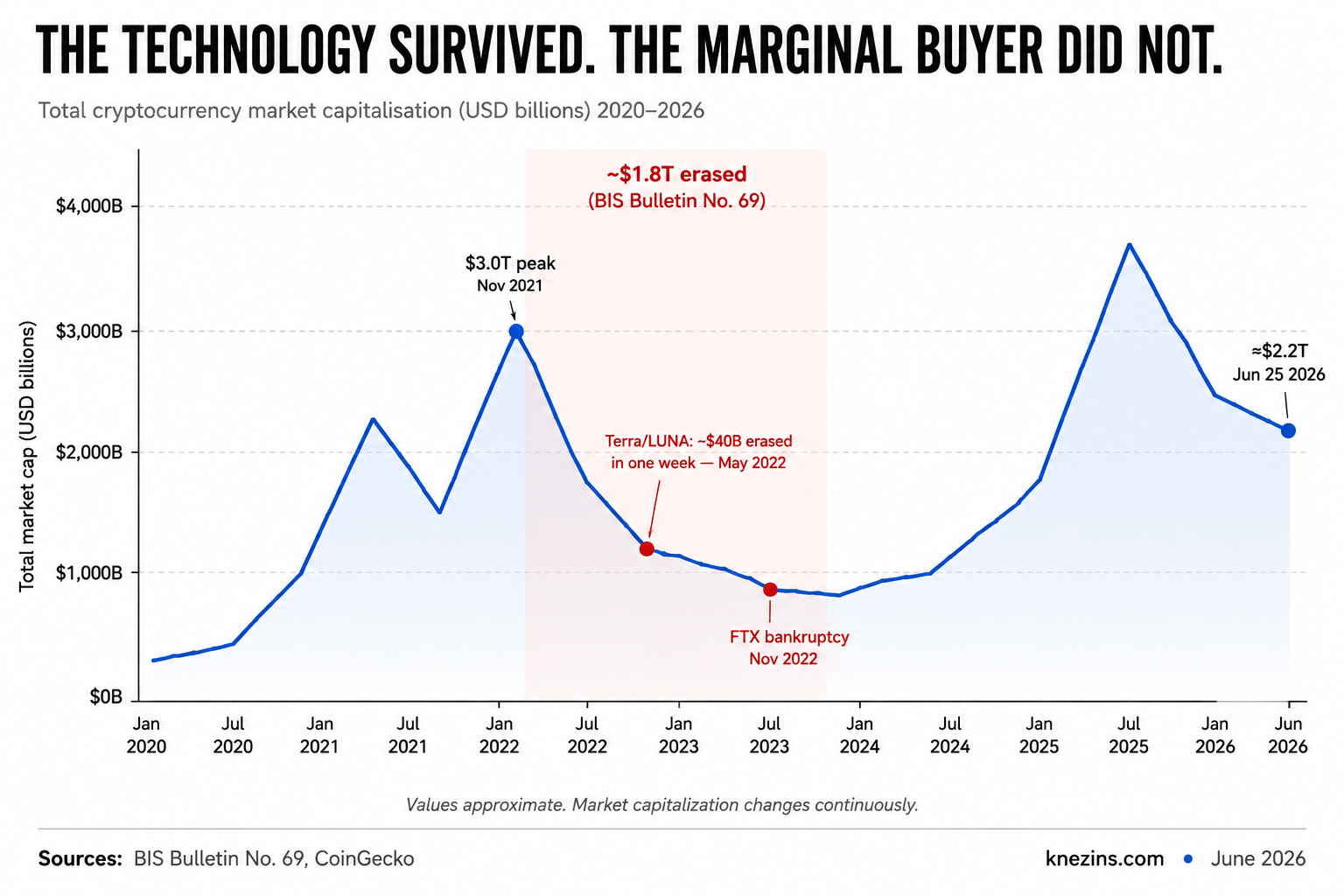

Total cryptocurrency market capitalisation USD billions 2020–2026. ~$1.8T erased 2022–2023.

His real superpower is not engineering. It is converting narrative into factories.

The crypto cycle repeats the dot-com lesson with one variation: the technology is more durable, the cycles are faster, and the gap between price and productive deployment is more visible in real time.

At $3 trillion peak in November 2021, the market had priced a financial infrastructure that did not yet exist at that scale. Terra/LUNA erased $40 billion in one week in May 2022. FTX collapsed in November the same year. The total market is still ~$2.19 trillion as of June 2026 — proof that the technology survived; evidence that the marginal buyer at peak did not always fare as well.

Elon Musk is described as an engineer, a visionary, a disruptor. All of these are partially accurate and mostly incomplete. The more precise description: Musk is an extraordinarily skilled capital allocator who has demonstrated, repeatedly, the ability to convert narrative into productive infrastructure. That is a rare and specific skill. Most people who are good at narrative cannot build factories. Most people who can build factories are not good at narrative. Musk operates at the intersection — and that intersection is where valuation multiples are born.

"I think it is important to reason from first principles rather than by analogy."

Elon Musk

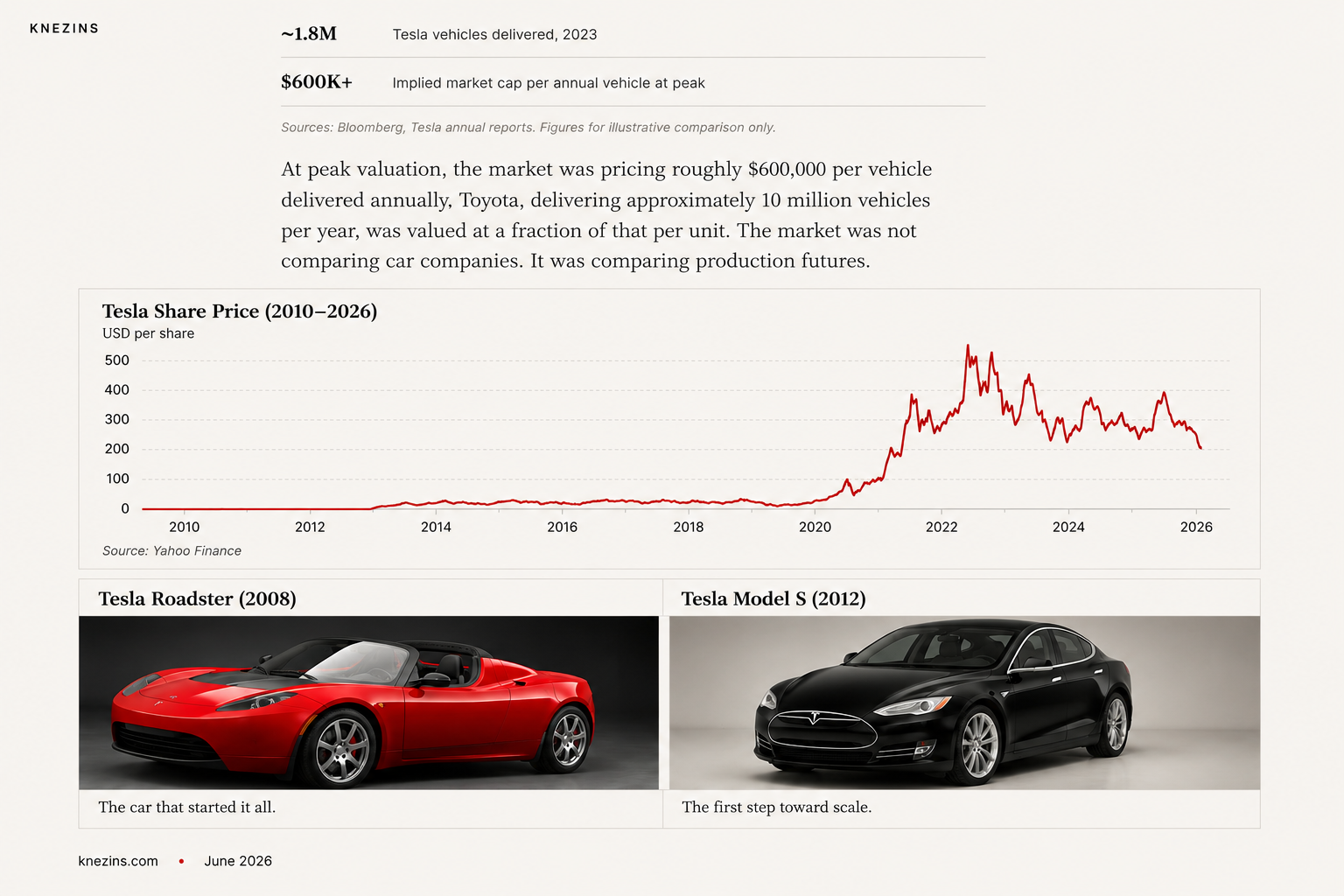

Tesla was not priced as a car company. It was priced as a manufacturing technology company that, currently, happened to make cars. The market was not buying Teslas. It was buying the belief that Tesla could build factories faster and more efficiently than any traditional automaker.

The market paid for future production capacity that had not yet been built. Whether it was right is still being decided.

~$1.1TTesla peak market cap, 2021

~1.8MTesla vehicles delivered, 2023

$600K+Implied market cap per annual vehicle at peak

Sources: Bloomberg, Tesla annual reports. Figures for illustrative comparison only.

At peak valuation, the market was pricing roughly $600,000 per vehicle delivered annually. Toyota, delivering approximately 10 million vehicles per year, was valued at a fraction of that per unit. The market was not comparing car companies. It was comparing production futures.

Tesla share price 2010–2026. Tesla Roadster (2008) and Model S (2012). The market was not buying cars. It was buying the belief in future production capacity.

Every trillion-dollar company is a bet on production that does not yet exist.

What the market is pricing

What exists today

Tesla — future manufacturing scale + energy + AI

Cars, energy storage, early autonomy. Real, but priced 5–10x forward.

NVIDIA — future AI compute infrastructure

GPU sales, data centre demand. Real revenue — priced for the decade ahead.

TSMC — irreplaceable future chip production capacity

The most defensible manufacturing moat in the world. Priced accordingly.

SpaceX — future launch economy + Mars + Starlink

Proven launch capability. Real Starlink subscribers. Mars economy: zero.

OpenAI — future AI output at civilisational scale

API access, enterprise agreements. AGI-scale output: not yet.

None of this means these companies are overvalued. It means their valuations are, in part, claims on production systems that must still be built. The question is not whether the technology is real. It always is. The question is whether the productive capacity implied by the price will materialise on the schedule the price assumes.

A higher price is not a larger economy.

When a factory is built, productive capacity increases. The economy can now make things it could not make before. Real output grows. This is wealth creation.

When an existing asset — a house, a share, a watch — changes hands at a higher price, a transaction occurs. The transaction is real. The wealth transfer is real. But the productive capacity of the economy may be entirely unchanged.

A rising market does not build a single factory, train a single engineer, or produce a single useful object. It is a claim on future production — valuable when that production arrives, painful when it does not.

The Capital → Production Loop:

↓

Moneyliquidity, policy, belief

↓

Capitalallocated to a vision

↓

Factoriesphysical capacity, built over time

↓

Productionrepeatable, scalable output

↓

Productsdelivered to real customers

↓

Cash Flowrevenue that validates the investment

↓

Valuationjustified by demonstrated output

The mistake is to shortcut from money directly to valuation — without passing through the middle. The middle is where the work happens. It is also where most projections quietly fail.

What if I'm wrong?

"Maybe markets are smarter than you think. They've correctly priced technological transitions before."

True. The market was right about the internet — just early by ten years. The argument here is not that markets are wrong. It is that the gap between price and production can be very wide, last very long, and cause significant damage to those who enter at the wrong point in the cycle.

"SpaceX is already generating real revenue. Starlink works. This isn't speculative."

Correct — and acknowledged. SpaceX has genuine operational capability. The argument is not that SpaceX is empty. It is that a meaningful portion of its valuation reflects a Mars economy that does not yet exist. Starlink revenue justifies a fraction of the reported valuation. The remainder is a production bet on a future that has not yet been built.

"Production timelines are compressing. AI, automation, and advanced manufacturing can close the gap faster than historical precedent suggests."

This is the strongest counterargument. The argument here is not that production timelines are fixed forever. It is that they have historically been more resistant to compression than market optimism assumes. The burden of proof remains on those who claim this time is structurally different.

One day, humans may walk on Mars.

When they do, they will not survive because someone priced the future correctly. They will survive because someone built it.

Brick by brick.

Factory by factory.

System by system.

In a place where no supply chain exists yet,

and every failure is potentially fatal.

Markets can price the future.

Governments can print money.

Investors can finance dreams.

Founders can articulate visions.

Engineers can solve the physics.

But nobody can print production.

Money can finance the future. Only production can build it.

About

Jānis Knēziņš

Born in July 1974 in Saulkrasti, Latvia. Lives in Garkalne.

For more than three decades, Jānis Knēziņš has built businesses and projects where execution matters more than presentation.

His work has taken him from Latvian forests and construction sites in Warsaw to the Sahara, Côte d'Ivoire, gold fields in Ghana, and cotton factories in Uzbekistan.

He writes about production, capital, systems, and the economics of building things that do not yet exist.

Today he is building JKNZ Studio while documenting the ideas behind production, value creation, and long-term thinking on this site.

The dreamers and the realists are usually different people. Not always.